23 May

Companies raise funds from different sources like issuing shares, borrowing from financial institutions, retained earnings, etc. Another main source of raising funds is through the issuance of debentures. The debentures are the funds borrowed by the company from the general public. As a result, it is a liability for the company, the discharge of this liability upon maturity is known as the redemption. Let’s learn more about the redemption of debentures, its methods and their journal entries.

Outline

What is a debenture?

What is the redemption of debentures?

Methods of redemption of debentures.

- Payment in Lump-Sum

- Payment in Installments

- Redemption Through the Purchase from Market

- Redemption Through the Conversion

Issue of debentures with the condition of redemption

What is Debenture?

Debenture is a form or format designed for long-term debt or loans that companies or firms use to borrow money from the general public or investors. Businesses and organizations issue debentures to raise funds for long-term activities and growth. Moreover, debenture includes how much money the investor gave, the interest rate, the maturity period, and the payment schedule.

What is Redemption of Debenture?

The repayment of any outstanding obligations and loans owed to the debenture holder or the lender who provided the loan is called the redemption of a debenture. In addition, it denotes the principal amount and the interest due to debenture holders.

In addition, debentures are typically redeemed at the end of their term by making payments to the debenture holders according to the terms and conditions mentioned in the debenture certificate. The liability will be discharged and removed from the balance sheet after payment.

Methods of redemption of debenture

The debenture redemption might take place in a variety of ways. Each of these methods has a unique accounting treatment. So, let us look at the various techniques of debenture redemption.

Payment in Lump-Sum

Redemption of debentures in lump sum occurs when the total amount of debentures is paid to debenture holders at one-time at maturity or even before maturity.

Because the corporation knows the due date in advance, it may organize its budget accordingly. As a result, the firm must prepare for such a debenture under the terms of the Companies Act and the SEBI rules. Debentures can be paid at par or premium according to terms decided during issuance of debentures.

Journal Entries

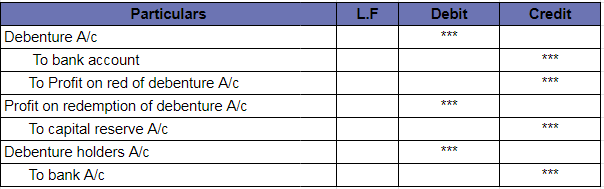

- In case of debenture redeemed at par

- In case of debenture redeemed at premium

- Redemption/Payment made to debenture holder

- If debenture redeemed out of profit

Payment in Installments

This method is also known as the drawing of lots. In this form of debenture redemption, the borrowed funds are repaid in a series of installments, which might be regular or irregular.

Journal Entries

- When debentures are redeemed out of profit

- When debenture are redeemed out of capital

Redemption Through the Purchase from Open Market

In this strategy, the corporation will purchase debentures from the open market and then cancel them immediately. The corporation might extend the maturity of the debenture until the payment is appropriate for its financial resources.

Journal Entries

- Debentures are purchased at a discount and canceled

- Debentures are purchased at price above nominal value

- 0wn debentures are purchased

- New shares are issued at par

Redemption Through the Conversion

The debentures are redeemed by converting them into fresh class debentures or shares in this method. The terms and conditions of such a debenture’s conversion are addressed to the holder when the debenture is issued. New shares or debentures can be issued at par, a premium, or a reduction at the time of conversion.

Journal entries

Debentures are redeemed at par

Issue of debentures with the condition of redemption

There are certain times when a company decides the conditions of redemptions immediately after issuing debentures. The debentures issued by the company may be at par, premium, or discount, but there are only two conditions for redemptions; at par and a premium.

The following six scenarios are frequent in practice, depending on debenture issuing and redemption terms and conditions.

Issue at par, redeemable at par

In this case, the debenture is issued at face value and will pay back to the debenture-holder at the same value, resulting in no profit and loss.

Illustration

A company issued 100; 8% debentures of $10 each. The amount is payable on application and redeemable at par after four years. Pass the journal entries.

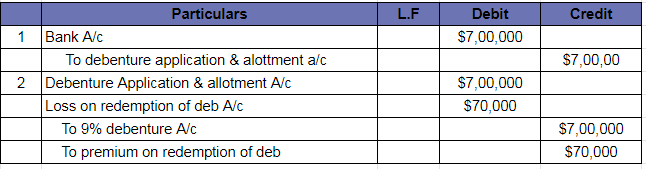

Issue at par, redeemable at premium

Debentures issued at par and redeemable at premium mean that the company will receive the total face value of the debentures and will refund the debenture with the premium at the time of redemption. Thus, it implies that the company will repay more.

Illustration

Party planners Ltd. issued 7,000; 9% debentures of $100 each at par and redeemable at a 10% premium. Give the journal entries for the issue of debentures.

Issue at discount, redeemable at par

Debentures are issued at a discount but redeemable at face value in this situation. This means the corporation will get less than the face value but redeem the entire face value.

Illustration

Company ABC issued 100; 9% of debentures at $50 at a discount of 8%, redeemable at par after 5 years. Pass the necessary journal entries.

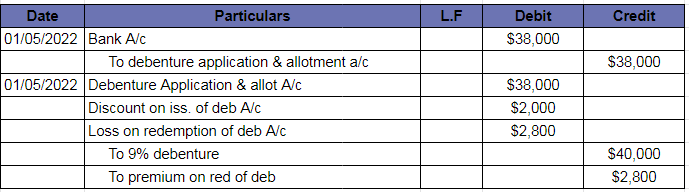

Issue at discount, redeemable at premium

In this case, the company issues debenture at a discount and promises to pay more than face value at the time of redemption.

Illustration

Green Ltd. issued 400; 9% debentures of $100 each on 1st May 2022. Pass the journal entries when the debenture is administered at a 5% discount, redeemable at a premium of 7%.

Issue at premium, redeemable at par

The debentures are issued at a premium in this case. This means that the company will receive more than the face value and will only return the face value upon redemption. As a result, the company will profit from the securities premium.

Illustration

Sultan madad & Co. Ltd issued 600; 9% debentures of $100 each at a premium of 5, redeemable at par. Give the journal entries.

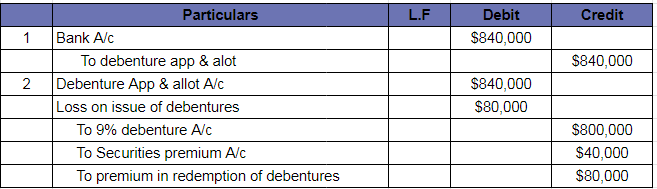

Issue at premium, redeemable at premium

In this case, the company issue debentures at a premium and redeem at a premium, which means that the company will get a profit at the time of debenture, but at the time of redemption, the company has to pay more.

Illustration

A company issued 8,000; 10% debentures of $100 each at a premium of 5% and redeemable at 10% after seven years. Pass the journal entries.

key Takeaways

- A debenture is a long-term debt or loan form or format used by companies or firms to borrow money from the general public or investors.

- Redemption of debenture is the repayment of any outstanding obligations and loans owed to the debenture holder or the lender who provided the loan.

- The different methods of redemptions are; payment by lump sum, installment, open market, and conversions.

Content writer at Invyce.com

Meena Khan