04 Apr

Cash basis accounting is fundamental to the accounting process which recorded the total revenue when cash is received. Cash accounting is all about cash transactions.

It is the simplest form to maintain accounting records, which is considered suitable for small businesses. While large size companies are advised to use the accrual basis of accounting for bookkeeping.

Table of content

- What is cash basis accounting?

- Cash basis accounting balance sheet example.

- Advantages and disadvantages of cash basis accounting.

- Cash basis accounting vs accrual basis accounting.

- Key takeaways.

What is cash basis accounting?

Cash basis accounting is an accounting process in which total revenue is recorded when cash is received and the company costs are recorded when they are paid. It is commonly used by individuals and small businesses.

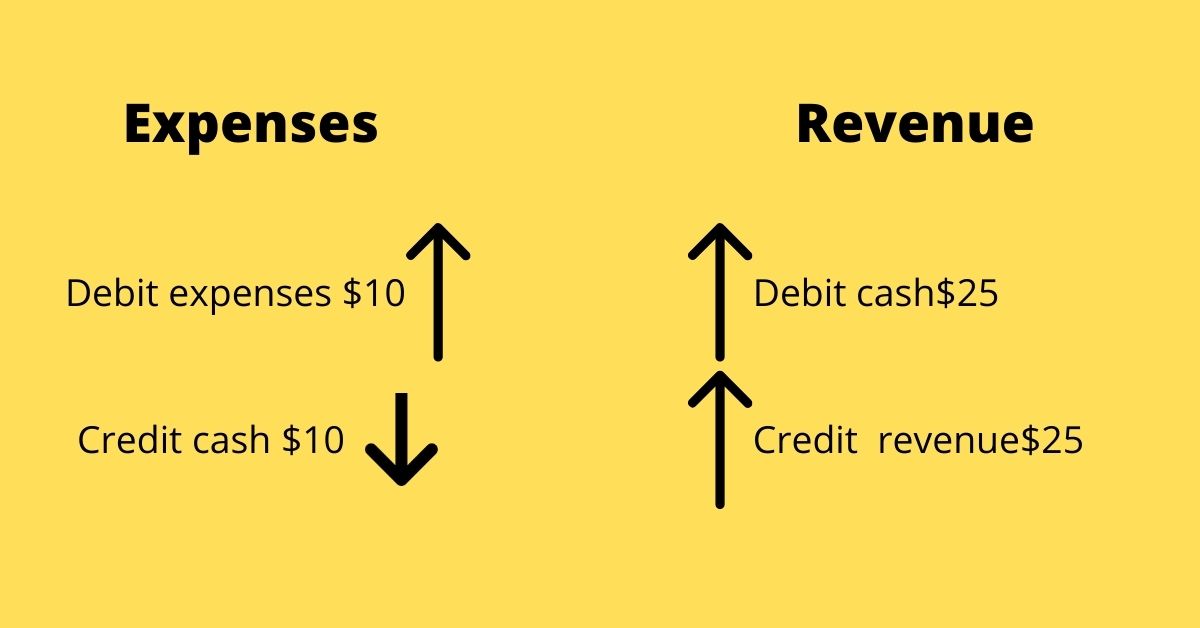

Let me elaborate on this with a simple example. Imagine you have got event management and a customer places an order for a birthday event. The material for this event cost you $10 to buy, and you have organized it at a 150 percent markup on cost so the customer pays you $25.

You have got two transactions to record. First, you need to record the expense, which in this case is the cost of buying the material for the event. You debit your expense by $10 to increase them, and you credit your cash by $10 for reducing your cash balance. You need to recognize your revenue which is the $25 that the customer pays you.

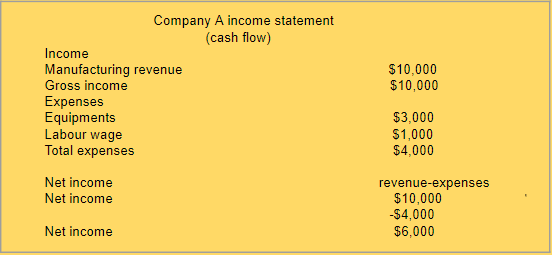

Let me elaborate on another example of cash accounting through the income statements.

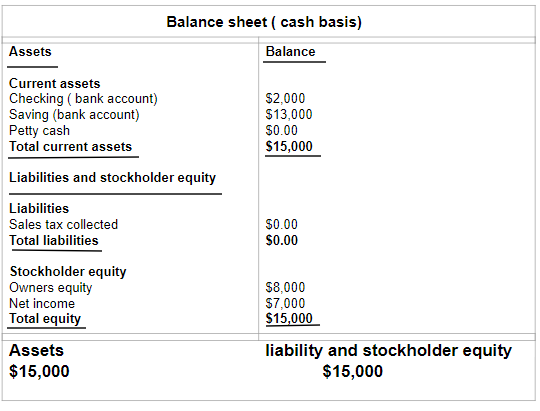

Cash basis accounting balance sheet example

In accounting, financial statements are used to collect and analyze financial data and the balance sheet is one of the important reports of financial statements. The three parts( assets, liabilities, and stockholder equity) are used to create a balance sheet with a cash basis accounting.

Accounting payable and receivable is not recorded in the balance sheet when you use the cash basis approach/method. As a result, unpaid bills and expenses are not reported. You have to keep a record on a separate sheet/document.

Let’s understand through example:

Advantages and disadvantages

Advantages

- It is simple to use and understand even for those with no or little transaction in accounting.

- This process can be done and maintained without any need for a qualified accountant.

- Liquidity- cash accounting is all about cash transactions. The potential investor who would like to invest in the business does not need to go through any liquidity ratio so he/she can look at the accounting system.

- Cash accounting is a single entry accounting which means that the effects only occur on a single account.. Business does not need to follow the matching concept principle which makes accounting transactions more simple to maintain and record.

Disadvantages

- It is not very accurate- since cash accounting only records cash transactions. cash accounting does not include all the transactions so as a result, we can say that cash accounting is not very accurate and under cash accounting, the expenses or revenue is recorded when the company pays or receives cash even in the different accounting periods.

- Not recognized by the companies Act- so few businesses follow cash accounting but it is not recognized in the companies Act as a result cash accounting is not practiced by the big companies.

- Chances of discrepancies- this is very important since cash accounting records the cash transactions, So there may be the probability that the business can be involved in unfair and malpractices by hiding the revenue or in fact inflating the expenses.

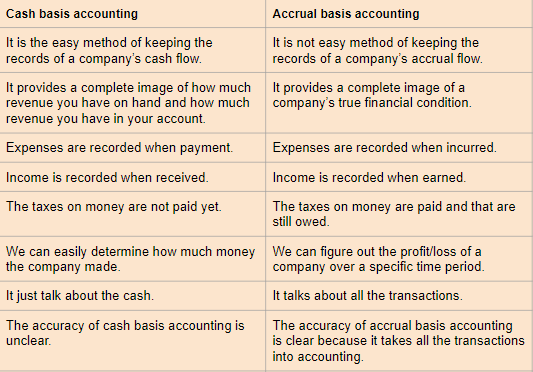

Cash basis accounting vs accrual basis accounting

Here I am going to discuss the differences between cash basis accounting and accrual basis accounting.

Key takeaways

- It is simple and easy to understand and keeps the records of a company’s cash flow.

- It is not as effective for large businesses or those with a lot of goods because it hides the underlying financial situation.

- Another form of accounting is accrual accounting, in which transactions are documented as income is made and expenses are induced, listless of whether or not money is exchanged.

- and does not capture the parts of the budget before cash is exchanged.

Content writer at Invyce.com

Seema Alam