| The debit account will record all the recipient accounts | The credit account is for the giver |

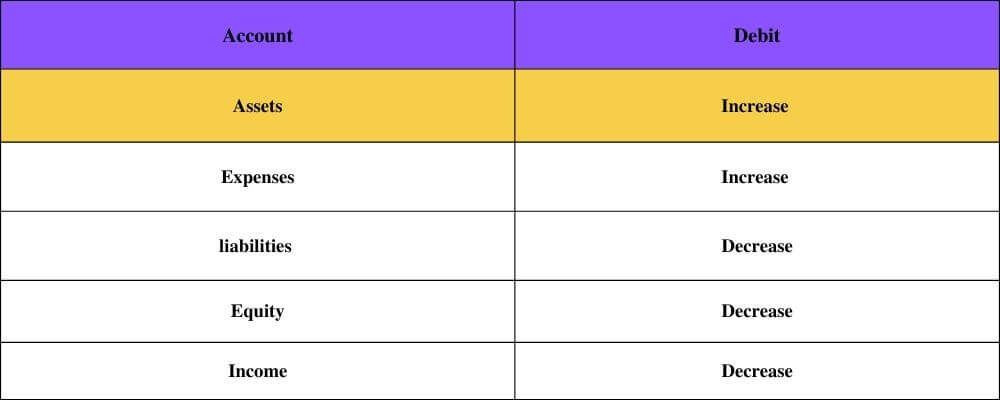

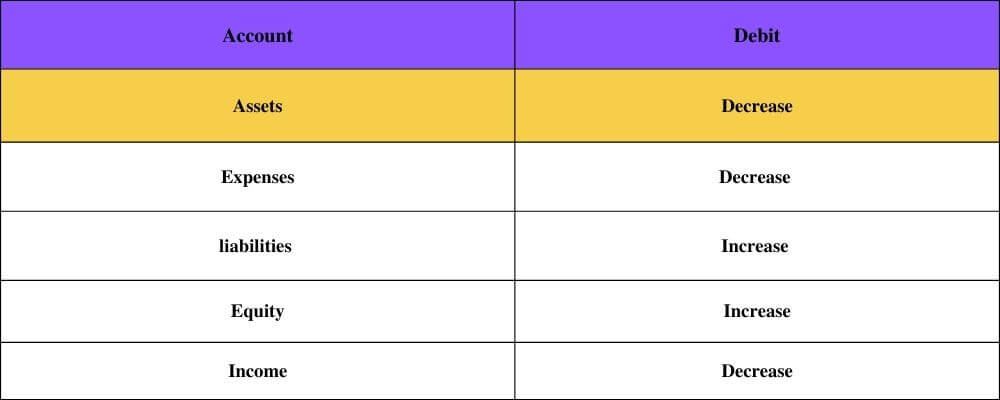

| Debit is used to record increase in asset and expense accounts and decrease in liability, equity and income accounts. | Credit is used to record decreases in asset and expense accounts and increase in liability, equity and income accounts. |

| In general journal account with a debit balance is recorded first |

Account with a credit balance is recorded by the following word “TO”.

|

Some major examples of the increase in debit is due to an increase in cash, inventory, equipment, machinery, building, land, insurance

| An increase in shareholder funds, retained earnings, sales, liability, and other causes an increase in credit.

|

Marjina Muskaan