08 Apr

It’s crucial to look at how companies use depreciation, which can account for a large number of a company’s owners on the financial report and have a short-term impact on the value of an opportunity to make money.

Depreciation is an accounting process that depreciates asset value over a period of time. The goal of depreciating an asset as a cost is to transfer the asset’s initial cost over its useful life.

You will find an in-depth insight in this article to fully understand the depreciation; types of depreciation method, accounting treatment of depreciation, and also accumulated depreciation versus depreciation expense with examples.

Table of content:

- Depreciation meaning

- What is depreciation in accounting

- Types of depreciation methods with examples

- Accounting treatment of depreciation

- Depreciation expense vs accumulated depreciation

- Key takeaways

Depreciation

Depreciation is the annual hidden and visible expenditure by an organization when employing capital costs like infrastructure, technology, or valuable equipment. It is the loss of a physical asset’s price.

The cost of the assets depreciates due to the regular use of strategic goals. Organizations use depreciation to account for the significance of the asset’s life. It is a fixed amount for businesses, and the money saved from depreciation can be utilized to buy new equipment after the old one is removed. As consequence, because it is a non-cash expense, it is considered a business expenditure.

What is depreciation in accounting?

In accounting, depreciation is the deduction of the actual cost of a lasting value in a methodical procedure till the asset’s value is zero. Depreciation is used by organizations to spread the expense of a real asset over time. There is no cash outflow during depreciation. Consequently, the cost is added to the collected depreciation in the accounting system. It is a major element of accounting that allows businesses to report the current book cost of real assets. The capital can also be spent to buy a new asset at a specific price. Let’s have a look at some of the terms included in depreciation.

- Cost of fixed assets

- Salvage value

- The useful life of fixed assets

- Rate of depreciation

In accounting, depreciation can be calculated through the different formula

- Depreciation= cost of fixed assets – salvage value / useful life of fixed assets

- Depreciation =( net book value – salvage value) ( rate of depreciation)

- Depreciation =(net book value – salvage value) (rate of depreciation) (2)

- Depreciation = (number of units produced in a given year) (depreciation rate per unit)

- Depreciation = ( useful life remaining / sum of years digits (100)) ( depreciable fixed assets value)

Types of depreciation methods with example

The value of all real assets diminishes over time. As a result, the organization/ company uses one of five techniques/methods to calculate the depreciation which is given below.

1- Straight line technique/method(SLM)

The straight-line method is the easiest method to calculate depreciation. It is a method of determining depreciation by charging a constant depreciation rate and amount throughout the useful life of the asset.

Depreciation= cost of fixed assets – salvage value / useful life of fixed assets.

The salvage value is the cost that the organization wants to collect when the equipment reaches to end of its useful life.

For example

Company ABC paid $20,000 for an asset that was estimated to be worth $2,500 at the end of its useful life. An asset’s projected useful life is five years. What is the appropriate depreciation for a company’s financial statement using the straight-line method?

Given

- Cost of assets = $20,000

- Salvage value = $2,500

- Useful life of assets = 5 years

Solution

Depreciation= cost of fixed assets – salvage value / useful life of fixed assets.

= $20,000 – $2,500 / 5 years

= $17,500 / 5 years

Depreciation = $3,500

So, the company charges depreciation of $3,500 in the financial statement Every year, hence the asset value decreases by $3,500.

2- Declining balance method (DBM)

The declining balance method is an annual depreciation methodology that charges depreciation on the net book value of an asset i.e value remaining after deducting depreciation from asset value in previous years.

Depreciation =( net book value – salvage value) ( rate of depreciation)

For example

Company ABC paid $20,000 for an asset that was estimated to be worth $2,500 at the end of its useful life. An asset’s projected useful life is five years. What is the appropriate depreciation amount for a company’s financial statement and what will be the depreciation expense when a company charges 20% per annum? Use the declining balance method.

Given

- Cost of assets = $20,000

- Salvage value = $2,500

- Useful life of assets = 5 years

- Depreciation rate = 20% per annum

Solution

Depreciation =( net book value – salvage value) ( rate of depreciation)

=($20,000-$2,500)(20%)

=($17,500)(20%)

=$17,500(20/100)

Depreciation amount = $3,500

So, after five years book value of a company is $5,888, and the depreciation will continue to charge in a similar pattern until the book value of the asset reaches zero.

3- Double declining depreciation method

This method is related to the decreasing/declining balance method, except it applies double depreciation expense to the amount of net book value of the fixed asset. As a result, it is regarded as an expedited/ accelerated approach.

Depreciation =(net book value – salvage value) (rate of depreciation) (2)

For example

Company ABC paid $20,000 for an asset that was estimated to be worth $2,500 at the end of its useful life. An asset’s projected useful life is five years. What is the appropriate depreciation amount for a company’s financial statement and what will be the depreciation expense when a company charges 20% per annum? Use the double-declining balance method.

Given

- Cost of assets = $20,000

- Salvage value = $2,500

- Useful life of assets = 5 years

- Depreciation rate = 20% per annum

- New depreciation rate = (2)(20%) = 40%

Solution

Depreciation =(net book value – salvage value) (rate of depreciation) (2)

=($20,000 – $2,500)(20%)(2)

=($17,500)(40%)

Depreciation =$17,500(40/100)

New depreciation amount =$7,000

So, after five years the net book value of a company is $1360.8, and the depreciation tends to apply to assets till their book value becomes zero.

4- Units of production method

The units of production method is a depreciation method in which the depreciable amount is divided by the total number of units the asset is expected to produce multiplied by the total number of units produced in the period, resulting in a depreciation expense of the depreciable amount divided by the total number of units produced in the period.

Depreciation rate per unit = fixed assets cost – salvage value / total number of units produced during the useful life.

Depreciation= Number of units produced in a given year X Depreciation per unit

For example

Assume a company purchased an asset worth $ 70,000a on January 1st and has a usage estimate of 40,000 hours. The equipment in question was operated for 6,000 hours in the first year. The salvage value is estimated to be $ 6,000.

Given

Costs =$70,000

Salvage value =$6,000

Total estimate production unit = $40,000

Solution

Depreciation per unit = ($70,000-$6,000) / 40,000 hours

Rate per unit = $64,000 / 40,000 hours

Rate per unit = $1.6 per hour

Below given is the hourly usage of the asset with respect to given years

- 6000 hours in 2016

- 8000 hours in 2017

- 9000 hours in 2018

- 11000 hours in 2019

- 7000 hours in 2020

5- Sum of years digits method

The sum of years digits method is a depreciation method that uses the whole number of useable years. In this case, the digits are arranged in descending sequence, and the sum of these numbers is calculated. The depreciation rate for the given year is calculated by dividing the total number of useable years by this sum and multiplying by 100. Finally, after subtracting the salvage value, the amount of depreciation is calculated by multiplying this percentage by the final fixed asset cost.

For example

A manufacturing company has purchased equipment for $50,000. The expense of transporting the equipment to their location was $20,000.The company believes that machines have a 3-year useful life and that they can dispose of them for $5,000.

Given

Total costs =$50,000+$20,000=$70,000

Salvage value =$5,000

Life of a equipment = 3 years

Depreciable fixed assets value = total cost – salvage value = $70,000-$5,000= $65,000

Solution

Depreciation = ( useful life remaining / sum of years digits (100)) ( depreciable fixed assets value)

Sum of years digits = 3+2+1=6

The first-year depreciation expense= $65,000(50%)=$32,500

Depreciation amount = $65,000-$32,500=$32,500

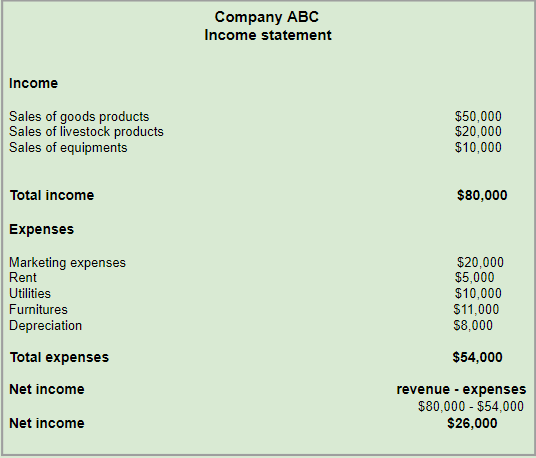

Accounting treatment of depreciation with example

Depreciation treatment in the income statement

Depreciation is reported in the income statement as a business expense and it is categorized as a non-cash expense because it does not result in real cash outflow. The business records the net cash expenditure/outflow for the total assets’ cost value when it is received/obtained. Let me elaborate on depreciation treatment in the income statement.

Suppose a manufacturing company purchases machinery for $50,000, the amount of salvage value of machinery is $10,000 and the expected useful life of machinery is five years. Calculate depreciation expense through the straight-line method.

Straight-line method = cost of an asset – residual value / useful life

SLM= $50,000 – $10,000 / 5 years

SLM = $40,000 / 5 years

Straight -line method= $8,000

Journal entry

.The depreciation is considered as an expense that is why we debit depreciation expense and credit accumulated depreciation as a contra asset account.

From journal entry we can, we can post accounts to their concerning financial statement. As depreciation expense is an item of the income statement and accumulated depreciation is of balance sheet item so, we can post depreciation expense to the income statement and accumulated depreciation to the balance sheet.

Hence we can say that the net income is equal to the revenue minus expenses( net income = revenue – expenses).

Accumulated Depreciation treatment in the balance sheet

A balance sheet is a form of financial statement that show the balances of assets, liabilities, and shareholder equity of a corporation at a specific time period. And can be used to assess a company’s cash flow assets and the debt to equity ratio.

Let’s have a look at below given balance sheet to analyze how accumulated depreciation is treated in the balance sheet:

Hence we can say that the total assets are equal to liabilities and shareholder equity( total assets = liabilities + shareholder equity).

Depreciation expenses vs accumulated depreciation

Depreciation expense and accumulated depreciation differ from each other in many ways. Let’s have a look at those differences.

Key takeaways

- Depreciation is the cost of utilizing a real asset with the advantage achieved over its useful life.

- Depreciation can be calculated through numerous methods, including straight-line and other types of depreciation.

- Salvage value is the amount realized from the sale of the asset after its useful life.

Content writer at Invyce.com

Seema Alam