11 Apr

In general, businesses or clients open a current account with a bank, conduct transactions, and record them in a bank column of their cashbook. In addition, the bank creates a separate account in its ledger for each firm or customer and provides a copy to the customer. The entries made in both the passbook and the cashbook do not always correspond. As a result, a statement is generated to identify the causes for the difference in the balances of both books as well as the overall balances, which is known as a bank reconciliation statement.

Table of Content:

- What is a bank reconciliation statement (BRS)?

- Purpose of bank reconciliation statement

- Why do differences occur between a bank statement and a company’s account?

- Benefits of BRS

- Steps in bank reconciliation

- Example

- The bottom line

What is a Bank Reconciliation Statement (BRS)?

A bank reconciliation statement is a report or statement prepared by a company as a result of a mismatch between the bank column of the cashbook and the bank statement. Its purpose is to reconcile bank transactions recorded in its books of accounts with that of bank statements. The statement details the deposits, withdrawals, and other transactions that have occurred in a bank account over a given time period.

Bank reconciliation statements are prepared to make sure that payments have been processed, and cash collections have been deposited in the bank. The statement aids in the identification of discrepancies between the bank and book balances, as well as the processing of necessary adjustments or repairs. Accountant processes reconciliation statements once a month to discover inaccuracies and correct them.

Purpose of Bank Reconciliation Statement

BRS is generated by customers of the bank on a regular basis to ensure that bank-related transactions are appropriately documented in the customer’s books of accounts and those of the bank. BRS assists in detecting inaccuracies in transaction recording. It also helps establish the precise document of bank balance as of a specific date.

Why Do Differences Occur Between Bank Statements and Company Accounts?

If you’ve been running a small business, you’ve probably seen discrepancies in records between the bank balance shown in companies’ books of accounts and the customer records kept by the bank. You may be asking why bank transactions recorded in the books of accounts do not match the bank statement. There are numerous causes for this, some of which are listed below:

- The company received or sent cash and cheques for deposit but not yet reflected in the bank statement.

- Banks collect fees on behalf of the company for services provided to clients.

- Certain types of bank accounts are subject to interest by banks.

- Banks can sometimes make errors while debiting or crediting transactions.

- Accountants can also make errors in accounting for bank transactions in books of accounts.

- Cheques were issued but not presented.

To eliminate such problems, you should create bank reconciliation statements. This statement simply compares the bank transactions in the company books with the bank statement. It ensures that the bank balance is always accurate in the books of accounts.

Benefits of BRS

- Bank reconciliation statements provide us with periodic checks and balances on both statements that can help you spot errors, omissions, and frauds.

- They aid in the detection of inaccuracies that may have an impact on tax and financial statements.

- If the company is confident in the accuracy of the cash book balance, it helps to secure future transactions with the bank.

- It can reveal any fraud committed by the bank or any other party. For example, if any employee shows any form of deposit in the bank but does not deposit it, you can disclose them by using this statement.

- A bank reconciliation assists you in detecting accounting problems that are frequent in all businesses. These errors include addition and subtraction errors, lost payments, and multiple payments.

- Banks may charge interest, fees, or penalties on your account. You can add or deduct such amounts from your records using monthly bank reconciliation.

- You might be able to prevent staff from stealing your money and also prevent it in the future. Bank reconciliation statements aid in the detection and identification of fraudulent transactions. To prevent the accounting employee from manipulating your accounts and reconciliations you should hire a third party.

Steps in Bank Reconciliation

Step#1:

The initial step in reconciling a bank statement is to compare the financial records of the company to those on the bank statement. These could be different due to different reasons.

Step#2:

The next step is to compare the credit side of the bank statement to the debit side of the cash book’s bank column, and the debit side of the bank statement to the credit side of the cash book’s bank column. Mark all the entries that appear in both records with a mark.

Step#3:

Examine the entries in both the cash book’s bank column and the passbook for entries that were missed to record in the cash book and passbook or whether there is any mistake in both of the records.t

Step#4:

If any inaccuracies, omissions, or errors are found in the cash book and pass book, correct or reconcile them. Then calculate the rectified balance of the bank column in the cash book.

Step# 5:

After making the necessary modifications and adjustments, compare the balances to check if they match. If not, go through the process again until you reconcile.

Example of Bank Reconciliation Statement

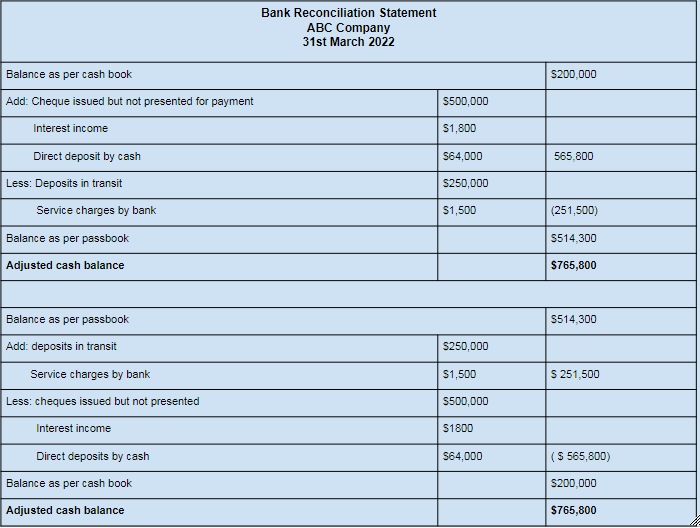

On 31st March 2022, the closing balance of the bank estimated in cash book of company ABC was $200,000. When they received the bank statement, to their surprise, the closing balance was $514,300. The company decided to prepare a bank reconciliation to reconcile bank transactions recorded in cash book and bank statement.

To create a bank reconciliation statement the company needs to identify transactions that result in a mismatch of bank balance in both of the statements.

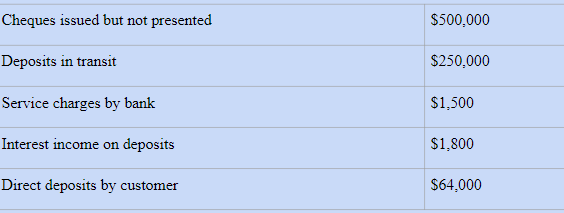

List of entries that make difference between cashbook and passbook;

After analyzing the differences between the company’s cashbook and bank statement, the following adjustments were done to the bank reconciliation statement.

The Bottom Line

A bank reconciliation statement compares the balance of the company’s accounts to the balance in the bank statement. It is a helpful tool for detecting errors, omissions, and fraud. When performed on a regular basis, BRS assists businesses in detecting fraud before major damage happens and preventing errors from compounding. It is also a simple and useful approach for managing financial flows.

Content writer at Invyce.com

Meena Khan