21 Mar

Financial statements are very essential while making several business decisions. Business owners, managers, and other stakeholders use financial statements to better understand the value and overall health of their company and to guide financial decision-making. The three financial statements; income statement, balance sheet, and cash flow statement, go hand in hand and provide complete information about the company’s financial status.

Table of content:

What are financial statements?

- Income statement — statement of operation

- Income statement formula

- Items of income statement

- Example of income statement

- What information income statement provide

- Balance sheet– statement of financial position

- Balance sheet equation

- Balance sheet items

- Example of balance sheet

- What information the balance sheet provides

3. Cash flow statement

- Example of cash flow statement

- The sections of cash flow statement

- What information cash flow statement flow

What are financial statements?

Financial statements are written reports that summarize the company’s financial performance and business activities during a certain period of time. Financial statements are an accurate picture of the financial affairs of the company. They are prepared by using financial data of the company collected by accountants and financial analysts by using standardized accounting principles. Investors, market analysts, and creditors use financial statements to assess a company’s financial health and profit potential. Financial statements have the goal of providing information about an enterprise’s financial status, performance, and changes in a financial position that may be used by a variety of users to make economic decisions.

The three main financial statements comprise an income statement, balance sheet, and cash flow statement.

Income statement— statement of an operation

Income statement is a financial statement that includes revenues and expenses, as well as the resulting net income or loss over time. It assists you in understanding the company’s financial health along with the balance sheet and cash flow statement. This document is being prepared to identify areas where expenses can be reduced and can generate more income. The income statement is also known as gain loss statements, earnings statements, and statements of financial results.

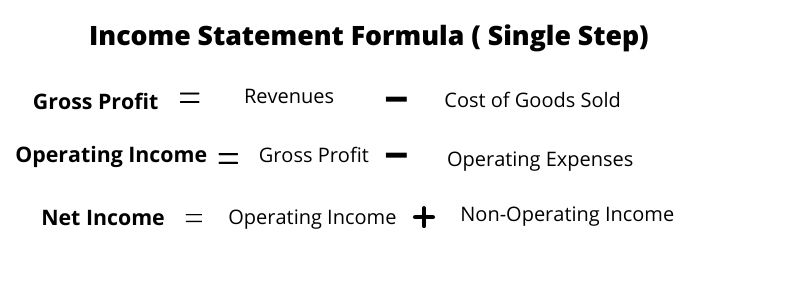

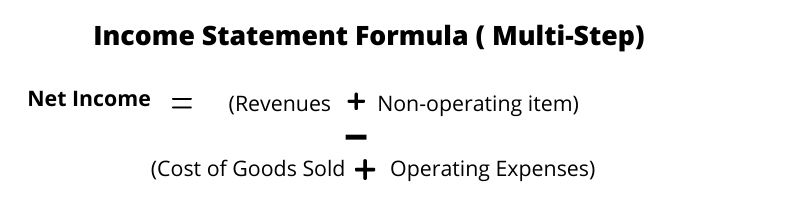

Income statement formula

Single-step income statement: In a single-step income statement only one category of revenue and one category of spending are shown.

The income statement formula under the single-step method is as follow;

Multi-step income statement: The multi-step statement divides expense accounts into more relevant and usable accounts.

The income statement formula under the multi-step method is as follow;

Items of income statement

- Net sales: The amount of money earned by a company from the goods sold is included in net sales.

- Cost of goods sold: This includes the cost you spent to purchase, produce products and services and sold by the company.

- Gross profit: Gross profit is net sale less cost of goods sold

Gross profit= net sale- the cost of goods sold

- Operating expenses: Operating expenses include the amount that the company spends during an accounting period. It includes salaries, rents, insurances, commissions etc.

- Net Operating Income: Net operating income represents the amount after deducting business operating expenses and taxes.

- Earnings before income tax: EBIT is the remaining amount after subtracting expenses from income before tax.profit before deducting income tax.

- Depreciation: Depreciation is a non-cash transaction that shows the value of assets of the company over a certain period of time.

- Net profit: It is the bottom line of the income statement and represents the final activities of a business. It is profit after deducting interest and income tax.

Example of Income Statement

| Company ‘A’ Income statement |

| Revenue $500,000 |

| Cost of goods sold ($4300) |

| Gross profit $495,700 |

| Operating expenses |

| Salary $7500 |

| Rent $600 |

| Printing and stationary $2300 |

| Refreshment $900 |

| Transportation $200 |

| Utilities $4300 |

| Total operating expense ($15,800) |

| Operating income $479,300 |

| Non-operating income |

| Interest $8500 |

| Commission $900 |

| Total non-operating income $9400 |

| Net profit before tax $488,700 |

| Tax ($400) |

| Net profit $488,300 |

What information income statement provides

- An income statement’s objective is to display a company’s financial success over time. It depicts the financial picture of a company’s operations.

- An income statement can tell you whether the company is profitable, whether it is spending more than it generates, when costs are highest and lowest, how much it costs to produce its product, and whether it has enough cash to reinvest.

- Accountants, investors, and business owners examine income statements regularly to determine how well a company is performing in comparison to its expectations and then utilise that information to change its actions.

Balance Sheet — Statement of Financial Position

The balance sheet provides a snapshot of a company’s financial status at any particular time. It is a document or report that lists a company’s assets, liabilities, and shareholder equity. The balance sheet also provides a broad picture of the performance of the company at a time, the company’s performance in the past, and the expected performance of a company in the future.

Balance Sheet Equation

An accounting equation is a basis for the preparation of a balance sheet ;

The assets of a company should always equal the sum total of liabilities and shareholder’s equity. A balance sheet is considered to be incorrect if the above equation is not balanced. In that case, the errors in a balance sheet are located and are corrected.

Items of balance sheets

Assets

Assets are resources and goods owned by a company that has value and can be converted into cash. Assets include all the cash owned by a company, all physical property (vehicles, plants, etc), and abstract things that have a value (trademark and patent).

Assets are further classified into current assets and non-current assets.

Current Assets

A company’s current assets are typically those that it plans to convert into cash or consume within a year. The most common current assets are as follow;

- Cash and cash equivalents: These are the most liquid forms of assets. They have a maturity period of fewer than 90 days and can be liquified on short notice.

- Marketable securities: All investments in debt and equity instruments that can be easily sold off in a liquid market are included in these assets. They can be converted into cash in 1 year.

- Account receivables: These assets include the amount owed by the customers of a company. The cash amount of the company increases when entities are able to recover the receivables.

- Inventories: Inventories includes all the work-in-progress, raw material and finished goods owned by a company. These are the assets that are expected to sell in the near future.

- Prepaid expenses: It includes all expenses that a company has already paid but has not used the services. The company is expected to get the services when needed. For example, advance salary paid to employees and insurance policies.

Non-current assets

Non-current assets can generate long-term financial gain and provide insight into the company’s operating performance. These are the assets that a company didn’t expect to convert into the cash in short term. They have a maturity period of more than one year. Non-current assets include;

- Plant, property and equipment: these assets include all the tangible items for example buildings, vehicles, equipment and land. These assets are relatively long-lived.

- Intangible assets: intangible assets include all the assets that can’t be seen or touched but have value. Patents, software and license are examples of intangible assets.

Liabilities

A liability is anything owed to another company or person by a company or organization. Liabilities include bills it has to pay, utility payments, debt payments, taxes, rents, etc. Obligations to provide goods or services to customers in the future also fall under the category of liabilities. Liabilities are classified into current liabilities and long-term liabilities.

Current liabilities

Current Liabilities are obligations owed by the company that must be paid within a specific accounting period, which is usually one year.

Current liabilities include;

- Account payables: Accounts Payable is an operating liability that the company must pay to its suppliers for goods and services received. It must be payable for the specified time period or in a year.

- Unearned revenue: It includes the revenue for which payment has been received but the service or product has yet to be delivered as of the balance sheet data.

- Short term debt: These liabilities include the loans that need to be settled within one year.

Long term liabilities

Long-term liabilities are obligations that aren’t expected to be settled within a year.

- Long term debt: long term debt includes long term loans and bonds issued by a company. When a business wants to raise money from outsiders to raise a fund for its operations or invest in new assets, it has a couple of options. It could seek a long term loan from banks or financial institutions who in return will expect to be repaid-with interest. Alternatively, businesses can also issue bonds. Bonds are similar to loans but they are raised directly from the public.

Shareholders equity

The word shareholder equity refers to a company’s net worth or the entire amount that would be returned to its shareholders if it were liquidated after all obligations were paid. The difference between Assets and Liabilities is used to compute shareholder equity, which is the shareholders’ residual interest in the company.

Example of Balance Sheet

The table below is a balance sheet of a fictional company. In the below example as you can see there are three sections of the balance sheet (assets, liabilities, and stockholder’s equity). Assets are at the top of the balance sheet followed by liabilities and stockholder’s equity. The value of total assets is $668,000 which equals the sum of liabilities and stockholders which means that this balance sheet is based on the balance sheet formula.

|

Company ‘A’ |

|---|

| ASSETS |

| Current assets |

| Cash and cash equivalent $3,000 |

| Short-term investments $15,000 |

| Accounts receivable-net $35,000 |

| Other receivable $2000 |

| Inventory $25,000 |

| Supplies $8,000 |

| Prepaid expenses $1000 |

| Total current assets $89,000 |

| Investments $30,000 |

| Property, plant & equipment-net |

| Land $6000 |

| Land improvements $8000 |

| Buildings $55,000 |

| Equipment $180,000 |

| Total property, plant & equipment $249,000 |

| Other assets including intangible assets $300,000 |

| Total Assets $668,000 |

| LIABILITIES |

| Current liabilities |

| Short-term loans payables $17,000 |

| Current portion of long-term debt $69,000 |

| Account payables $30,000 |

| Income tax payables $26,000 |

| Other accrued liabilities $5,000 |

| Deferred revenues $30,000 |

| Total current liabilities $177,000 |

| Long-term liabilities |

| Notes payable $15000 |

| Bonds payable $11,500 |

| Deferred income taxes $114,500 |

| Total long-term liabilities $141,000 |

| Total liabilities $318000 |

| STOCKHOLDERS EQUITY |

| Common stock $185, 000 |

| Retained earning $250,000 |

| Accum other comprehensive income $15,000 |

| Less: treasury stock ($100.000) |

| Total stockholder’s equity $350,000 |

| Total liabilities & stockholder’s equity $668,000 |

What information does the balance sheet provide?

- Balance sheets give the user a quick overview of the company’s assets and liabilities.

- The balance sheet is a vital instrument that executives, investors, analysts, and regulators use to assess a company’s current financial health.

- The balance sheet is used to compare the entire amount of debt to the total amount of equity. This data is particularly valuable for lenders and creditors who want to know if extending more credit may result in bad debt.

- Investors use a balance sheet to examine whether enough cash is available to pay their debts or other payables.

- Users can also use the balance sheet to determine whether a business has a positive net worth, whether it has adequate cash and short-term assets to pay its obligations, and whether it is heavily indebted in comparison to its rivals.

Cash Flow Statement

A cash flow statement is one of the important financial statements that show how much money enters and exits your business over a specific time period or during an accounting period. It provides us with information about the cash you have on hand for a given period. While income statements also show us how much money you’ve spent and earned, however, they don’t always tell you how much cash you have on hand at any given time. The cash flow statement provides insight into the various areas in which a business used or received cash; it is an important financial statement when valuing a company and understanding how it operates.

Example

To get visualised information about cash flow statements take a look at the example of the cash flow statement of a fictional company.

|

Statement of Cash Flow CASH AND CASH EQUIVALENTS, BEGINNING OF THE YEAR $6500 |

| OPERATING ACTIVITIES Net income $4500 Additions to cash Depreciation $500 Increase in Account Payables $6500 Subtraction from Cash Increase in Account Receivables ($5,000) Net Cash from Operating Activities $6,500 |

| INVESTING ACTIVITIES Equipments $3000 |

| FINANCING ACTIVITIES n/a |

| CASH FLOW FOR MONTH DEC 31, 2021 $9,500 |

The above cash flow statement shows variations in cash for a reporting period that ended on December 31, 2021. The opening balance of cash and cash equivalents was approximately $6500, as you’ll notice at the top of the statement.

During the Accounting period, operating activities generated a total of $6500. In investing activities no cash is spent on debt and equity financing activities. At the bottom of the cash flow statement, the final balance of cash and cash equivalents at the end of the year is 9500.

The sections of a cash flow statement

The cash flow statement comprises three statements that show us different ways cash can enter or leave the business.

Cash flow from operating activities

Cash flow from operating activities is money earned or spent in the course of regular business activity. These activities may include purchasing and selling inventory and supplies, as well as paying employees’ salaries. Other types of inflows and outflows, such as investments, debts, and dividends, are excluded.

Cash Flow from Investing Activities

Cash flow from investing activities is the amount of money earned or spent on investments made by your company, such as purchasing equipment or investing in other businesses. Cash spent on property, plant, and equipment is also included in this section. This is the section where analysts look for changes in capital expenditures (Capex).

Cash flow from financing activities

Cash flow from financing activities is cash earned or spent while financing your business with loans, lines of credit, or shareholder’s equity. It is a measure of cash flow between a company, its owners, and its creditors, and it is typically derived from debt or equity. The cash flows from the financing section are used by analysts to determine how much money the company has paid out.

What information does cash flow provide?

- The cash flows statement provides a more detailed picture of what happens to a company’s cash during an accounting period.

- Cash flow statements are used by business owners, managers, and other stakeholders to better understand the value and overall health of their companies and to guide financial decision-making.

- Cash flow statement show changes in assets, liabilities, and equity as cash outflows, cash inflows, and cash held. These three activities are the core of any business management.

- Cash flow statements can be used to generate cash flow projections, allowing you to forecast how much liquidity your company will have in the future. This is critical when developing long-term business plans.

Conclusion

Each financial statement has its own purpose and provides specific information, but together they are the most powerful tool and provide all the financial information.