23 Mar

Closing journal entries are an essential component of the accounting cycle in which balances from temporary accounts are transferred to permanent accounts.

Let’s learn about the purpose, types, significant steps, and examples of closing journal entries.

Moreover, the companies must close their books at the end of each fiscal year to prepare their annual financial statements and return tax.

However, most companies prepare monthly financial statements and close their books annually. As a result, they have a full clear picture of company performance during the year and give users timely information to make decisions.

In this article, we have discussed closing journal entries, such as for purposes, objectives, and steps of closing journal entries.

Table of content

- What are closing entries?

- Explanation of temporary and permanent account

- Purpose of the closing entries?

- Objectives of closing entries

- Four-step in preparing closing entries

- Conclusion

What are closing journal Entries?

A closing journal entry is a journal entry that is made at the end of an accounting period to transfer the balance from a temporary account to a permanent arrangement.

ABC company

Adjusted Trial Balance

January 31, 2020

| Date | Account | Debit | Credit | |

| Jan 31 | Service revenue | 85,600 | ||

| Income summary | 85,600 | |||

| Jan 31 | Income summary | 77,364 | ||

| Wages expenses | 38,200 | |||

| Supplies expense | 18,480 | |||

| Rent expenses | 12,000 | |||

| Phone expenses | 1,494 | |||

| Electricity expenses | 2,470 | |||

| Miscellaneous expenses | 3,470 | |||

| Interest expense | 150 | |||

| Depreciation expenses | 1,100 | |||

| Jan 31 | Income summary | 8,236 | ||

| Retained earnings | 8,236 | |||

| Jan 31` | Retained earnings | 5,000 | ||

| Dividend | 5,000 |

Explanation of Temporary and Permanent

Accounts

Temporary Accounts

Temporary accounts are known as nominal accounts i.e., expense, revenue, gains, and losses, the balance of these accounts should be zero before starting the next accounting period—the most common accounting period for small businesses is one year.

Temporary accounts are the accounts in the general ledger that are used to accumulate transactions over a single accounting period. The balance of these accounts is eventually used to construct the income statement at the end of the fiscal year.

Four types of temporary

There are four main types of temporary accounts to prepare financial statements. However, every kind of account has its own function.

- Expense:

The expense accounts measure the money that the company spends on the performance of its operation. As a result, the account balance will increase each time the company spends funds, creating a negative amount that sets off revenue in the loss and profit calculation.

- Revenue:

The revenue account measures the cash or receivables the company earns through selling its goods and services to customers. As a result, it contributes a positive amount to the profit and loss calculation and has a credit balance on the trial balance.

- Income summary

The income summary is a temporary account created purely to close temporary accounts. It is the total running of all your revenue and expenses.

At the same time, all account statements must be reset to zero at the end of the accounting period. To this, their balances are emptied into the income summary account.

Moreover, the income summary account then transfers the net balance of all the temporary accounts to retained earnings which is a permanent account on the balance sheet.

- Dividends

Business owners use a dividend account to distribute part of profit against shareholding. This is a distribution of the company profits to the business owner.

Permanent Accounts

Permanent accounts are those accounts that continue to maintain an ongoing balance over time. All accounts are aggregated into the balance sheet.

Permanent accounts are the accounts that show the long-standing financial position of a company. For example, balance sheet accounts are permanent accounts. These accounts carry forward their balance throughout multiple accounting periods.

Example of Permanent Account

Permanent accounts are those accounts that are reported on the balance sheet. They include assets accounts, capital accounts, and liability.

Assets Accounts

Assets accounts such as cash, account receivable, prepaid expenses, inventories, fixtures, furniture, etc., are all permanent accounts.

Liability accounts

Liability accounts are accounts payable, notes payable, rent payable, interest payable, loans payable, utilities payable, and other payables are permanent accounts.

Capital Account

Capital accounts of all types of businesses are permanent accounts. But this includes the owner’s capital account in a sole proprietorship, partners’ capital accounts in partnerships, reserve accounts capital stock, and retained earnings in corporations.

Purpose of Closing Journal Entries

The closing journal entries are used to transfer the contents of the temporary accounts into the permanent account, retained earnings, which resets the temporary balances to zero, further enabling tracking of revenues, expenses, and dividends in the next period.

A term often used for closing journal entries is reconciling the company’s accounts. At the same time, accountants perform closing entries to return the revenue, expenses and temporary account balances to zero in preparation for the new accounting period.

The closing entries are recorded so that the company’s retained earnings accounts show any actual increase in revenues from the previous year and any decreases in dividend expenses and payments.

Retained earnings are not distributed to shareholders as dividends but retained for further investment, often in advertising, sales production, and types of equipment.

| Items | Debit | Credit |

| cash | 5,000 | |

| Prepaid rent | 10,000 | |

| Accounts payable | 3,000 | |

| Accounts receivable | 25,000 | |

| Common stock | 1,000 | |

| Income tax payable | 6,000 | |

| Salaries accrual | 5,000 | |

| Retained earnings | 0 | |

| Dividends | 5,000 | |

| Rent expense | 14,000 | |

| Revenue | 70,000 | |

| Salaries expense | 20,000 | |

| Income tax expense | 6,000 | |

Process of Closing Entries

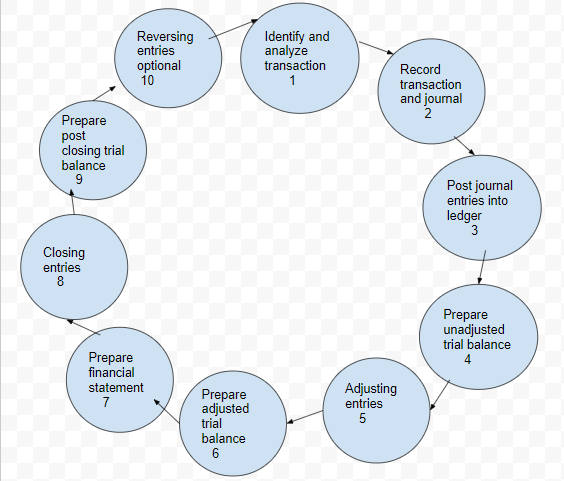

Closing journal entries are eight steps in the accounting cycle. In this step, accountants close temporary accounts of the current accounting period so that new accounts should be maintained in the new accounting period.

This step closes temporary accounts into permanent accounts by following a procedure discussed below.

1. Close revenue account

Transfer the balance of all the revenue accounts to the income summary account. It is done by debiting multiple revenue accounts and crediting income summary accounts. This step closes all revenue accounts.

| Account | Debit | Credit |

| Revenue | 70,000 | |

| Income summary | 70,000 |

2. Closing expenses account

Transfer the balance of various expense accounts to an income summary account. However, It is done by debiting income summary accounts and crediting multiple expense accounts. This step closes all expenses accounts.

| Account | Debit | Credit | |

| Income summary | 40,000 | ||

| Rent expense | 14,000 | ||

| Income tax expense | 6,000 | ||

| Salaries expense | 20,000 |

3. Closing income summary account

At this point, you have closed the expense and revenue accounts into an income summary. But the balance in the income summary represents $70,000 credit and $40,000 debit, which shows there is a $30,000 credit balance. Does that number seem familiar?

The income summary should match the net income from the income statement. At the same time, we want to close this credit balance by debiting the income summary.

What did we do with net income? We added it to the retained earnings in the statement of the earnings retained.

| Account | Credit | Debit |

| Income summary=70,000-40,000 30,000 | 30,000 | |

| Retained earnings | 30,000 | |

If expenses are greater than revenue, we would have a net loss. But a net loss would decrease retained earnings, so we can do the opposite in this journal entry by debiting Retained Earnings and crediting Income Summary.

4. Closing dividends account

After we add net income or remove net loss on the statement of retained earnings, what do we do next? We close dividends to get the ending balance of retained earnings. This journal entry will be a form of doing this calculation but be careful because you do not want to use the amount of retained earnings but dividends. However, We want to decrease retained earnings debit and close the balance in dividends, for doing that we credit to the dividend account and debit retained earning account.

| Account | Debit | Credit |

| Retained earnings | 5,000 | |

| Dividend | 5,000 |

Retained earning (credit balance)=beginning balance+credit entries-debit entries

=0+30,000-5,000

Retained earning =$25,000

Conclusion

The closing entries occur at the end of an accounting cycle as a set of journal entries. While closing journal entries, suit to transfer the balances out of certain temporary accounts into permanent ones. this resets the balance of the temporary accounts to zero, ready to begin the next accounting period.

Marjina Muskaan has over 5+ years of experience writing about finance, accounting, and enterprise topics. She was previously a senior writer at Invyce.com, where she created engaging and informative content that made complex financial concepts easy to understand.

Marjina Muskaan