19 May

Do you know? Businesses use different methods to maintain good financial health. Most use income statements cash flow statements, balance sheets, and other reports to accurately report financial statements. But a statement of changes in equity is not considered an essential tool by many businesses, they neglect and carry on with another one.

The interesting thing you should know is that the statement of change in equity is essential because it can add context to other financial statements. It helps shareholders to see what influences gains or losses in equity throughout the accounting period that can further inform their investment strategy. Here I will discuss the statement of change in equity statement and how to prepare it.

Table of content

- What is the statement of change in equity

- Statement of change in equity formula

- How to prepare the statement of change in equity

- Importance of statement of changes in equity

- Key takeaways

Statement of change in the equity

It is the financial statement that reports the change in the equity from net income (loss), owner investment/contributions, and withdrawals over a period of time. In simple words, the Statement of change in equity reports the opening balance and closing balance of the owner’s equity

This is a shorter financial statement, and there aren’t many transactions that directly affect equity. However, it provides accurate information on how equity moves through the business reporting period (usually one year). It can also identify the par value of common treasury stocks that build investor trust in your company. It covers the following elements.

- Owner’s equity

- Net profit and loss

- Equity withdrawals

- Dividend payments

- Treasury stock purchase

- Effects of change in fair value on assets

- Effect of correction of errors in a prior period

Statement of owner’s equity formula

This formula provides you with a clear idea of what you need to include in your statement.

Opening balance of equity +net income-Dividends +/-other changes=closing balance of equity.

Preparing the statement owner’s equity

The statement owner’s equity carries the company name at the top and the date for which the statement prepare. Thus, the statement processes begin with the net/opening equity, adding net income with the opening balance of equity and subtracting dividends and other adjustments to get the closing balance of the period.

Here is the format of the statement of owner’s equity with examples.

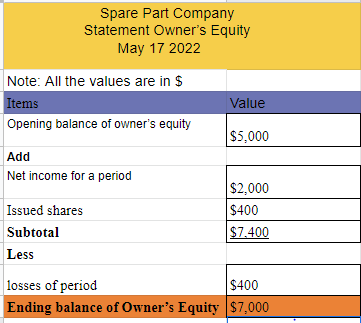

Example # 1

Suppose a company of spare parts which has an opening balance of owner’s equity is $5000 as of January 2021. The company raises money from equity investors worth $400; within the year, the company also generates a net income of $2000.If there were some losses from some non-operating activities worth $400, then the company will get an ending balance of owner’s equity.

Prepare a company’s Statement of Owner’s Equity.

Example # 2

John has a company John Traders. The owner’s equity is $50,000 at the beginning of reporting period, i.e. January 2021. Now John traders paid dividends of $5000. During the period, a company earned a net income of $5000.

Though the company never losses, John wants money urgently for an unwarranted situation. Hence, he makes a withdrawal of $4000 from the capital account.

Prepare a statement of owner’s equity of John Traders.

Here is an explanation of items in the owner’s equity statement

Opening balance

It is the ending balance of the previous year’s statement of shareholders of equity. All the addition and subtraction of the current financial year occur in the equity statement.

Net income

Net income/net earnings is the total earning of income in the fiscal year.

Other incomes

All the additional income earned by a company, such as actuarial or unrealized gains from financial instruments.

Issue of a new capital

It is an inflow of capital or an addition to the shareholder’s equity. It adds to the shareholder’s total equity.

Net loss

Net loss is a total loss by the company during the fiscal year. The net loss deducts from the statement of the owner’s equity.

Other losses

All the additional losses by the company are not recognized in the income statement and are accounted for in the equity statement, such as actuarial or unrealized losses from financial derivatives.

Dividends

A dividend is a reward that company shareholders earn on their investment in the company’s share. It reduces the shareholder’s total equity and deducts it from the owner’s equity statement.

Withdrawal of capital

When capital is withdrawn from the company. It is deducted from the equity shareholder’s statement and reduces the total equity of the company.

Importance of Statement of changes in the equity

The statement of equity shares provides detailed information about changes in the equity share capital over an accounting period that is not reflected/shared somewhere in the financial statements. Therefore, such statements are helpful for the shareholders and investors to make effective decisions regarding their investments.

Key Takeaways

- Hence, the statement of change in equity gives you the movement of equity from one accounting period to the next.

- It begins with the net/opening equity, adding and subtracting items over time such as profit and dividend payment to get the closing balance of the period.

- The statement of equity shares provides detailed information about changes in the equity share capital over an accounting period that is not shared somewhere in the financial statements.

Shabana has been a committed content writer and strategist for over a 5 years. With a focus on SaaS products, she excels in crafting compelling and informative content.

Shabana