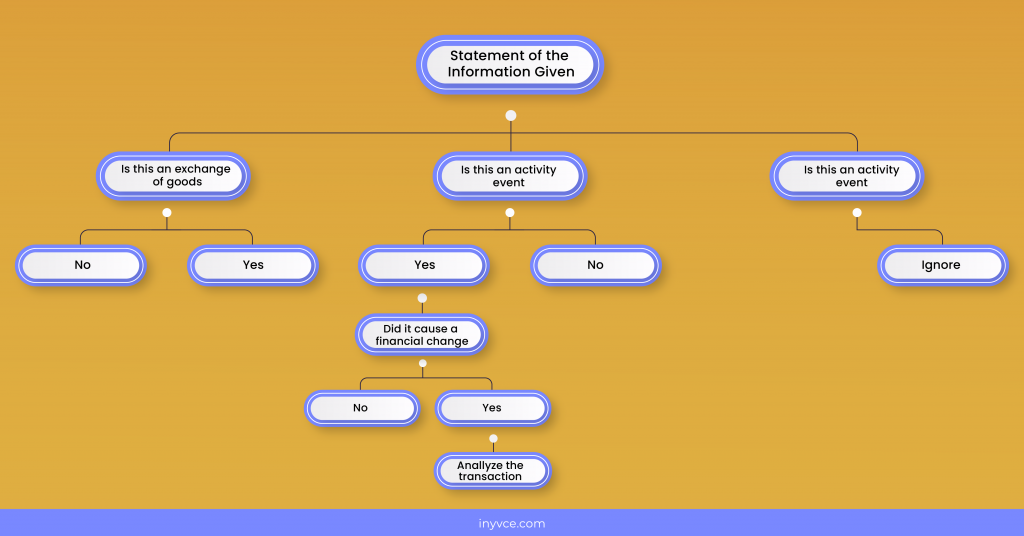

Identify If the Event is an Accounting Transaction

First, you need to determine whether this transaction is a business-nature transaction. An accounting transaction has to involve cash because only signing a contract can not be considered a transaction, and it must require making a payment to consider it an economic event or transaction. Examples include the sale of products, the purchase of equipment, and salary payments.

Identify what Accounts it Affects.

The second step is to identify which accounts the Transaction will affect. For example, John invested $100,000 in a business and purchased a truck with a market value of $ 50,000.

The cash invested will be capital. The truck purchase will be an asset for that business. The accounts impacted by transactions are capital, truck, and cash accounts.

Identify what Accounts it Affects.

Every Transaction results in a measurable change in the accounting equation. Knowing whether the account belongs to asset, liability, or equity will let you know to identify whether the account will have debit or credit balances. In the above example, we determined that the accounts involved are Asset accounts, i.e., truck and cash, and the capital account is the Owner’s Equity account.

Identify which Accounts are Going up or Down

A business uses debit and credit effects to record any transaction. These double-entry procedures keep the accounting equation in balance. So when John invests cash, the capital and cash account increase because, at this stage, money, and capital are coming into the business. On the other hand, when a truck has been purchased, truck(asset) accounts will increase, and cash(asset) account will decrease.

Apply the rules of Debits and Credits to the Accounts

Every business must record transactions in two or more related but opposite accounts. Therefore, we debit one account and credit the other in the same transaction amount.

We apply golden rules of accounting to record these transactions, accounts on the left side increase with a debit entry and decrease with a credit entry, while accounts on the right side increase with a credit entry and decrease with a debit. So, if the plant and machinery account increases, which is an asset account, it will be debited to show an increase in assets. While to show the increasing effect of equity, we record on the credit side of an entry.

Find the Transaction Amounts to be Entered

The last step of analyzing transactions is to identify the amounts to be recorded on the debit and credit sides of an entry. For example, in the above example, if capital was invested Rs.10,00,000, then debit will be given to the cash account with Rs.10,00,000, and credit is given to the capital account with the same amount.

Marjina Muskaan